Kaspi.kz (NASDAQ: KSPI)

A Kazakhstan super-app at single-digit earnings. The first foreign large-cap to clear the Microcap Investing Checklist with documented scope carve-outs.

DATE : May 26, 2026

TICKER : NASDAQ: KSPI

PRICE : $93.00 USD

MARKET CAP: ~$17.77B USD

In this article we examine Kaspi.kz (NASDAQ: KSPI) — a Kazakhstan-headquartered fintech and super-app, the only foreign large-cap position in a portfolio otherwise built from Canadian microcaps, and the largest holding in the book. This article explains why I broke my own framework to hold it.

I missed this name for nearly two years. KSPI’s NASDAQ debut in January 2024 was at approximately $87 per ADS. I watched it trade. It briefly fell to $68 in mid-2025 on Hepsiburada integration fears. I did not buy. By the time my work was complete the price had recovered to $93. The opportunity here was not finding KSPI before the market did — it was being prepared to do the work when the mispricing was already visible on the screen.

Part 0: The Business Blueprint

Kaspi.kz operates the dominant mobile application in the Republic of Kazakhstan. The app integrates three operating businesses into a single consumer relationship: payments, marketplace, and fintech lending. Munger would call it a Lollapalooza — multiple independent systems converging on the same competitive outcome.

The Engagement

15.7 million Monthly Active Users in Kazakhstan, against an adult population of ~13 million — a saturated, single-app market.

10.7 million Daily Active Users — a DAU/MAU ratio of 68%, described in the 20-F as among the highest engagement metrics of any mobile application globally.

77 transactions per active consumer per month — roughly 2.5 times a day.

764,000 active merchants accepting Kaspi Pay.

47% brand recognition versus 8% for the #2 app, per a KResearch survey of 6,000 Kazakhstan respondents.

We are describing the WeChat of Kazakhstan in everything but name.

The Three Loops

Payments: ~1.0-1.1% blended take rate across peer-to-peer transfers, bill pay, merchant QR-code acceptance, and B2B payments. 95% of merchants use Kaspi Acquiring; 85% of consumers pay household bills through the app. The low-monetization loop whose job is to create the daily habit.

Marketplace: Third-party e-commerce, e-grocery, classifieds (Kolesa.kz for cars and Krisha.kz for real estate, each #1 in country at 74% brand awareness), travel, advertising, and last-mile delivery via 10,441 Postomat lockers. Take rate climbed 9.7% (2024) → 10.5% (FY 2025) → 12.1% (Q1 2026). 49% of orders arrive within two days; 84% delivered free.

Fintech: BNPL (41% of lending), general-purpose loans, automotive finance through Kolesa, and merchant/SMB finance. Loan book KZT 7.2 trillion (~$15 billion USD). Underwriting completes in under six seconds, 99.9% automated. Cost of Risk stable at ~2% across cycles. NPL ratio 6.1%.

The loops feed each other. Payments creates the trust and transaction data. The data underwrites the lending book. The lending book funds Marketplace purchases via BNPL. Each loop strengthens the next.

The Türkiye Expansion (Hepsiburada)

In January 2025 KSPI closed the acquisition of an 86% stake in Hepsiburada, Türkiye’s longest-running e-commerce platform, for approximately $1.1 billion. Türkiye is now ~26% of consolidated revenue. The thesis is to port the Kazakhstan playbook to an 85-million-person market. First-year metrics are encouraging: Hepsiburada orders moved from -11% YoY in Q1 2025 to +19% by Q4 2025.

In March 2025 KSPI signed to acquire the Türkish banking subsidiary of Rabobank N.V., expected to close mid-2026. In Q4 2025 the company launched Kaspi Alaqan — pay-by-palm biometric authentication; in Almaty alone, 511,000 consumers (roughly one-third of the city’s adult population) registered within three months, with Kazakhstan-wide rollout through 2026.

The Moat: The Saturation Floor

The moat is daily-use saturation. Once an entire country runs its payments and credit through one app, the competitor’s customer-acquisition math collapses. Displacement requires rebuilding the daily habit of 15.7 million people, one consumer at a time, against a 47%-versus-8% brand-awareness gap. No domestic competitor has attempted this; no international competitor has the local regulatory licensing or merchant network to make it economical.

I will call this The Saturation Floor — the level below which the business cannot fall without literally rebuilding that habit. The Türkiye expansion compounds value on top of it; the Kazakhstan home market defends it from below. Every analytical decision that follows is anchored to this concept.

Part 1: The Gatekeepers (The Kill Switch)

These are the four universal filters of the checklist. If KSPI fails any single one, the analysis terminates.

1. TFSA Eligibility — PASS

Rule: The security must be listed on a CRA-designated stock exchange to be eligible for a Tax-Free Savings Account.

Audit Finding: PASS.

2. Anti-Commodity / Sector — PASS

Rule: Operating business with revenue. No shells, no pre-revenue lottery tickets, no commodity producers, no single-product biotechs.

Audit Finding: PASS. FY 2025 consolidated revenue KZT 4.05 trillion (~$8 billion USD) across Payments, Marketplace, and Fintech segments. Not extractive, not pre-revenue, not subject to single-product approval risk.

3. Customer Concentration — PASS

Rule: No single customer above 20% of revenue, unless the relationship is a structural lock-in.

Audit Finding: PASS. Concentration is structurally below 0.1%.

B2C platform: 15.7 million Monthly Active Users in Kazakhstan plus 11.8 million Hepsiburada consumers in Türkiye. No single end-consumer represents a material share of revenue.

4. Earnings Quality — PASS

Rule: No going-concern qualification, no restated financials, no material related-party revenue, CFO greater than 50% of NI for three consecutive years, accruals not growing faster than revenue for four-plus consecutive quarters.

Audit Finding: PASS on all five sub-criteria.

Going-concern: Deloitte issued a clean audit on March 13, 2026 — no warnings, no caveats. The one item the auditors flagged is how KSPI estimates loan-loss reserves, which is standard for any bank.

Restatements: None. No auditor changes either.

Related-party revenue: 0.097% of total revenue (same figure as the Customer Concentration check above).

Cash flow vs reported profit: Cash from operations covered 130% / 55% / 63% of net income in 2023 / 2024 / 2025 — all above the 50% threshold the rule requires.

Loan-loss reserves vs revenue: Loan-loss provisions grew 43% (2024) and 42% (2025) against revenue growth of 32% and 60%. Provisions outpaced revenue in only one year out of four — not the four-quarter pattern the rule actually flags.

Forensic Insight: KSPI discloses one material weakness in internal controls. The headline sounds worse than it is.

The Kazakhstan core business has effective internal controls — confirmed by both management and Deloitte. The material weakness applies only to Hepsiburada (the Türkiye acquisition), which is excluded from the controls assessment under the standard first-year SOX carve-out. Hepsiburada is about 4% of consolidated assets and 25% of revenue.

The actual issues are gaps in Hepsiburada’s IT systems and process documentation — inherited at acquisition, remediation already in progress. Not revenue-recognition fraud. Not accounting gamesmanship. The kind of issue that gets cleaned up over the integration period.

This is the “external panic, franchise intact” pattern: the headline reads alarming, the underlying business is fine.

Part 2 : Track A Classification — The Compounder Path

[X] A1. Solvency — PASS (deposit-taking translation)

Rule: The standard checklist test is cash and short-term investments greater than total debt. But KSPI is a bank, and for a bank that test doesn’t fit cleanly — customer deposits aren’t really “debt” in the operational sense. They’re how the bank funds its loan book. The right version of the test for a deposit-taking business is non-deposit debt against liquid resources, plus a capital adequacy check.

Data: At Q1 2026, KSPI holds about KZT 2.32 trillion in liquid resources (~$4.85 billion USD). That’s a net liquid position of roughly $3.6 billion USD excluding customer deposits. Tier 1 capital adequacy under Basel III (administered by Kazakhstan’s central bank) sits well above the regulatory minimum.

Verdict: PASS under the bank-translation test. Customer deposits of KZT 6.8 trillion are funding for the loan book, not debt to be netted against cash.

Forensic Insight: The April 2026 Eurobond settlement is the most important balance-sheet event of the past twelve months. KSPI raised $600 million in its debut international Eurobond issuance, settled April 24, 2026. International lenders willing to fund KSPI at competitive emerging-market spreads is third-party validation of the credit profile the equity market is currently underpricing. International lenders willing to fund KSPI at competitive emerging-market spreads is third-party validation of the credit profile the equity market is currently underpricing.

[X] A2. Profitability — PASS

Rule: Profitable in each of the last three fiscal years, with Return on Equity above 20%.

Data: FY 2025 net income was KZT 1.068 trillion (~$2.1 billion USD). KSPI has been profitable every year since its London Stock Exchange listing in 2020 and in every year before that under predecessor accounting. Return on Equity (averaged over the year) was approximately 51% in FY 2025 — down from roughly 79% in FY 2024 and 86% in FY 2023.

Verdict: PASS DECISIVELY. The drop in ROE through 2025 isn’t a deterioration of the business — it’s the math reacting to the Hepsiburada acquisition. When you absorb a company that big, your equity base swells, which mechanically drags the ROE ratio down even if the underlying business hasn’t weakened. ROE excluding the Türkiye consolidation is still in the 70-80% range.

Forensic Insight: A drop in ROE the year of a major acquisition is mechanical and expected. The real question is whether the acquired business produces enough incremental return on the capital spent to recover the dilution over time. The first-year Hepsiburada signal is encouraging — orders moved from -11% year-over-year in Q1 2025 to +19% by Q4. The integration is tracking ahead of plan.

[X] A3. Dilution — PASS

Rule: No meaningful growth in share count over the last five fiscal years. Convertible debt, warrants, and at-the-money issuance programs evaluated for future dilution risk.

Data: Diluted share count over five years: 192.19M → 190.31M → 189.33M → 190.02M → 190.23M. That’s a net change of about -1% — meaning a slight cumulative net buyback, not dilution. No convertible debt outstanding. No warrants. Executive equity compensation is paid in shares that vest over five years, with a board-discretionary clawback that can reduce up to half of the CEO’s exercisable equity if performance disappoints. KSPI also ran a $100 million share buyback program between November 2025 and February 2026 at an average price of KZT 39,150 per ADS (~$77.50), deploying $43 million of the authorization.

Verdict: PASS. The dilution profile is one of the cleanest in the global super-app cohort.

Forensic Insight: The CEO clawback in the executive comp plan is a Munger-grade incentive alignment construct — the CEO’s exercisable equity can be cut by up to half for underperformance, at the discretion of the board’s compensation committee. That’s real skin in the game: not just the upside, but real downside if execution misses.

[X] A4. Valuation — PASS

Rule: Price/Earnings ratio below 15x on a trailing-twelve-month basis. PEG ratio below 1.0 against forward earnings growth.

Data: At the current price of $93.53 per ADS, KSPI trades at 7.82x trailing P/E (per stockanalysis.com, accessed May 26, 2026). PEG against FY 2025 underlying net income growth of 18% comes to 0.43. PEG against Q4 2025 underlying growth of 13% comes to 0.60. Both well below the 1.0 threshold.

Verdict: PASS. The cheapest member of the comparable super-app cohort by a wide margin.

Forensic Insight: The conservative 2026 management guidance (~5% Adjusted EBITDA growth) is artificially compressing forward PEG estimates that use the guidance number as the denominator. The guidance is depressed for three identified, temporary reasons:

Kazakhstan raised the corporate tax rate on banks from 20% to 25% effective January 2026.

Kazakhstan’s central bank raised minimum reserve requirements in August 2025 and again in April 2026.

A one-time smartphone import-supply disruption in early 2026.

None of these reflect deterioration of the underlying business. They’re all known headwinds that flow through the income statement but don’t change the franchise economics.

Part 3 : The Quality Scorecard

The 8-factor Scorecard ranks the candidate against the existing top-five holdings in the portfolio. KSPI passes seven of the eight items cleanly; the eighth — Institutional Gap & Liquidity — is set aside under documented scope.

1. Sales Velocity (>20% YoY) — PASS. Q1 2026 consolidated revenue +31% YoY. FY 2025 underlying revenue +21%. e-Commerce revenue Q1 2026 +58%.

2. Quality Floor (ROE >20%) — PASS DECISIVELY. ROE 41-51% depending on whether the calculation uses ending or average equity. Either reading is more than double the threshold.

3. Unit Economics (gross margin >40-50%) — PASS with the segment lens. Payments segment Adjusted EBITDA margin Q1 2026 ~57%. Fintech segment ~37%. Consolidated gross margin appears lower because interest expense on customer deposits is in operating costs rather than below the gross margin line — a structural artifact of bundling banking and consumer technology under one income statement.

4. Momentum (within 20% of 52-week high) — PASS. Current $93.53 within the 52-week range of $68.59-$99.20. Currently 5.7% below the 52-week high. The stock rallied off the mid-2025 low as the Q1 2026 results validated the early Hepsiburada integration.

5. Inflection Signal — PASS. Multiple identifiable catalysts in motion: the Türkiye/Hepsiburada engagement gap closing (orders -11% Q1’25 to +19% Q4’25), the Rabobank A.Ş. acquisition pending closing mid-2026, the Kaspi Alaqan rollout Kazakhstan-wide, the April 2026 Eurobond settlement providing funding flexibility, and potential NBK rate cuts in the second half of 2026 explicitly NOT included in guidance.

6. Institutional Gap & Liquidity — N/A SCOPE CARVE-OUT. This factor exists to identify names before institutional money arrives. KSPI is post-discovery. Documented carve-out, not a failure.

7. Intelligent Fanatic — PASS. CEO Mikheil Lomtadze co-founded the company, has been at the helm for approximately twenty years, and owns 22.62% personally. Chairman Vyacheslav Kim, also a co-founder, owns 20.78%. Harvard Business School has published two case studies on the build.

8. Promotion Test — PASS. The Q1 2026 and FY 2025 CEO letters to shareholders discuss Türkiye expansion economics, Hepsiburada engagement metrics, the Rabobank rationale, Alaqan rollout, NBK and Ministry of Finance regulatory headwinds, and the interest rate cycle. Neither letter mentions the share price.

Total Quality Score: 7 of 8 items pass cleanly; 1 item set aside under documented scope. Final classification: Compounder.

Part 4: Financial Forensics — Why KSPI Is Cheap

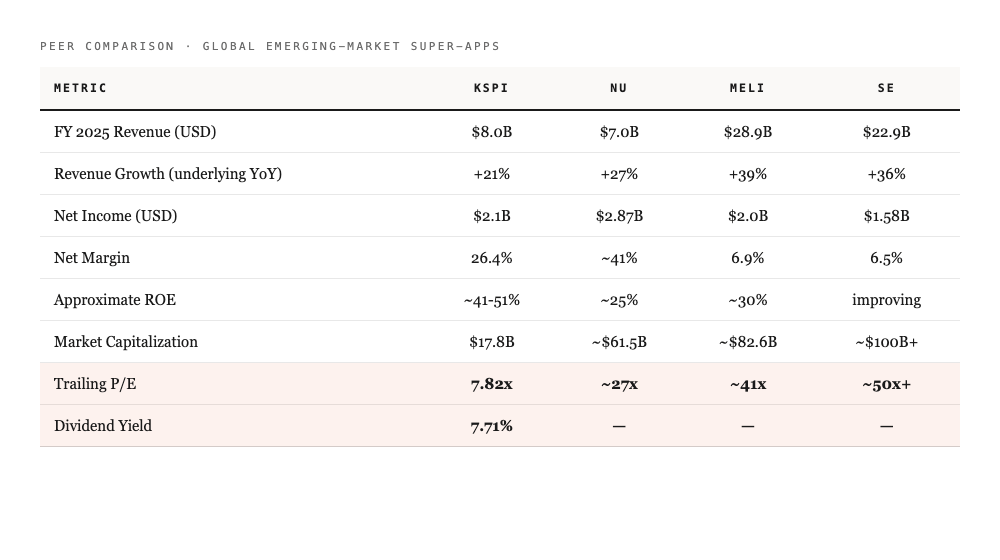

The fastest way to test whether KSPI is mispriced is to compare it against companies running the same business in other markets. The peer group is the global emerging-market super-app cohort: Nu Holdings (NU), MercadoLibre (MELI), and Sea Limited (SE). Each runs the same payments + commerce + lending architecture in a different country.

KSPI is the cheapest member of the peer group on Price/Earnings by a factor of three to six. It’s also the highest in the group on Return on Equity and net margin. And it’s the only one paying a meaningful dividend — a 7.7% trailing yield on a 64% payout ratio against growing earnings.

Two ways to look at the valuation. Both say the same thing.

The first is a standard DCF. Using a 10% discount rate, 3% terminal growth, and net income compounding at 12% a year for ten years, the model puts fair value around $281 per ADS against today’s $93.53. Run the math with a 12% discount rate and you get ~$200. Run it with 2% terminal growth and you get ~$240. The DCF doesn’t need to be right at any specific number — it just needs to bracket reality. Across any reasonable set of assumptions, fair value is at least double the current price.

The second is a strategic takeout test: what would someone pay to buy KSPI outright? Emerging-market fintech and super-app acquisitions over the last decade have changed hands at 15x to 25x Adjusted EBITDA in private deals. KSPI’s FY 2025 Adjusted EBITDA was $3.08 billion USD. At 15x: $46 billion enterprise value. At 18x: $55 billion. Even after taking a 30% haircut for emerging-market geopolitical risk, you land at $32-47 billion versus today’s $17.77 billion EV.

Both lenses point the same direction.

Three reasons KSPI is cheap — all of them temporary.

The wrong-passport discount. A Kazakhstan-listed issuer trades into a perceptual emerging-market discount in the United States that doesn’t reflect the business quality. A large chunk of the U.S. mutual fund universe can’t hold the security by mandate or because of ADR liquidity rules. Structural in the short term, time-limited in the medium term.

The Hepsiburada overhang. Reported earnings compressed in 2025 because Hepsiburada was managed near Adjusted EBITDA breakeven by design during the integration year. Reported ROE fell from ~86% to ~51% because the equity base inflated from the acquisition — not because the business deteriorated. As the integration normalizes through 2026 and 2027, reported numbers converge back toward underlying economics.

The Kazakhstan regulatory ratchet. The corporate tax rate on banks rose from 20% to 25% in 2026. The NBK raised minimum reserve requirements in August 2025 and April 2026. Each tightening compresses the Fintech segment’s profitability mechanically. Real, but a one-time step-down — not a structural margin decline.

Every one of these drivers is temporary, identifiable, and already in the current price. None of them argues that KSPI is a worse business than its peers. They argue KSPI is the same caliber of business trading at a Price/Earnings ratio one-fifth of the peer average. That gap is the variant perception.

Part 5: The Risks and Where I Stand

Four things could break the thesis. Here they are, with what mitigates each.

Russia exposure — the actual kill case. Kazakhstan shares a 7,600 km border with Russia and runs significant cross-border trade. In April 2025 a class-action lawsuit was filed in the Supreme Court of New York alleging that KSPI’s January 2024 IPO disclosures understated Russia exposure. KSPI filed a motion to dismiss in August 2025; the ruling is still pending. If the Russia-Ukraine conflict escalates and Kazakhstan financial institutions become secondary-sanctions targets — or are even perceived to be at risk — KSPI could face deposit flight, ADR liquidity compression, and material legal liability.

Mitigation: KSPI’s actual operational revenue exposure to Russia is small. The perceptual risk is bigger than the operational risk — but if perception flips, the stock takes the hit before the operational facts catch up. This is the position-killer. It’s why position sizing is set against The Saturation Floor scenario.

Hepsiburada — the wildcard. Over $1 billion was deployed in January 2025 to buy 86% of a Türkiye e-commerce platform whose standalone profits deteriorated as KSPI invested for growth. First-year integration metrics are encouraging, but Türkiye is a more competitive market than Kazakhstan was at the equivalent stage (Trendyol has ~30M users). Lira inflation runs 30-70% chronically, distorting the financial reporting. The pending ~$300M Rabobank A.Ş. acquisition layers another Türkiye banking-license bet on top.

Mitigation: Türkiye is an upside option, not the core thesis. The Kazakhstan home market alone supports today’s enterprise value. The downside is a Hepsiburada write-down — painful, but the franchise floor holds.

The Kazakhstan consumer credit cycle. The loan book grew 23% YoY in Q1 2026 against an NPL ratio that rose from 5.4% (FY 2024) to 6.1% (FY 2025). Cost of Risk ticked up from 0.6% to 0.7% in Q1 2026. Most of the loan book is unsecured consumer credit. Kazakhstan’s 2022 Citizens Bankruptcy Law opened individual debt write-off avenues that didn’t exist before. A real credit crunch could spike NPLs into the 10-15% range.

Mitigation: Underwriting is automated and tightening in real time. Q1 2026 saw a deliberate slowdown in new loan acceptance. Cost of Risk has averaged ~2% across past credit cycles — the long-run figure to watch.

The NBK regulatory ratchet. Bank corporate tax rose from 20% to 25% in 2026. Reserve requirements stepped up twice. Each tightening mechanically compresses Fintech-segment profitability.

Mitigation: Already in conservative 2026 guidance. Payments and Marketplace aren’t affected by the bank tax. The diversified business model absorbs the Fintech-specific drag.

The case against the case is that these four risks are correlated. A Russia escalation widens the wrong-passport discount, increases sanctions risk for Kazakhstan banks, and dampens the consumer credit cycle — all at once. A failed Hepsiburada integration becomes both an earnings drag and a write-down. The bear case isn’t four independent factors. It’s one geopolitical thread pulling on all of them. Position sizing is set against that scenario.

Where I stand.

I’m long KSPI as the largest position in the portfolio. Position size is matched to the Russia kill case — if it materializes, the position takes the perceptual hit without breaking The Saturation Floor.

I’m not adding at the current price. The position is correctly sized, not under-sized. I’m not trimming. The thesis re-validates every quarterly print.

The next data point is the Q2 2026 release in mid-August. Two things I’m watching: (1) does Hepsiburada’s order growth sustain through Q2 (the recovery from -11% in Q1’25 to +19% in Q4’25)? (2) does the NPL trajectory stabilize, or does the credit cycle accelerate?

The Steal Price. Three tiers:

$75-$85 — initiation zone for a new investor building a full position from zero.

Below $90 — add-on trigger for the existing position, assuming the Q2 print validates Türkiye and the credit cycle stays orderly.

Current $93.00 — still attractive for new initiation with conviction. The full thesis applies at this level, with 53-67% margin of safety to documented fair value ($200-$281) and a 7.7% dividend yield while the gap closes.

The Microcap Investing Checklist exists to focus capital where individual retail investors have an edge. KSPI is the first foreign large-cap to pass the analytical layer with documented scope carve-outs. The carve-outs are documented. The Saturation Floor is the anchor. The work is on the record. Future exceptions to the funnel scope will need to clear the same bar.

Disclosure

I am long KSPI. I am not a registered investment advisor. This is not investment advice. Do your own work.

The audit is the work. The verdict is yours.

Thanks P-A! On the position — I've never actually held Kidoz, it was research coverage, so no change there.

You might be onto something, though. The dip to a loss isn't the business weakening — it's the opposite: they're deliberately reinvesting, putting real money into the AI / Prado build-out while revenue keeps growing. That's a company spending today to be bigger tomorrow, and if it pays off there's a genuine chance this becomes a really good business. Definitely one worth watching closely here.

Brilliant Research !